This is part 3 of the money priorities where we analyze Dave Ramsey’s 7 Baby Steps.

For those who have not read the first part where we looked into Baby Steps 1-2 and Baby Steps 3-4.

Step 5: Save for your children’s college

When it comes to saving for your children’s college education, it’s a topic that can evoke different opinions and personal circumstances. If you don’t have children or don’t believe in financially supporting their education, you can proceed to the next step. It’s valid to question the return on investment of sending your child to college, especially considering the stories of students graduating with substantial student loan debt for degrees they may not even pursue a career in.

However, personally, I lean towards the value of a college degree and the overall impact it can have on a child’s personal growth and development.

To save for your children’s education, opening a 529 plan is often the recommended approach. These plans offer tax advantages for education expenses and have expanded their definition of qualified expenses over time.

In my case, I opted for Fidelity’s 529 plan as it provided me with more investment options, such as the S&P 500 index, compared to some plans with limited fund choices.

Determining how much to contribute to a 529 plan is not limited by specific restrictions. You’re essentially making an educated estimate based on a few factors: A) your child’s inclination to attend college, and B) the projected cost of college education, keeping in mind that your child could be just a few years old.

While there’s no one-size-fits-all answer, it’s worth considering the importance of having some savings set aside for your children’s educational aspirations. It provides them with opportunities and flexibility, should they choose to pursue higher education in the future.

Step 6: Pay off your home early

In Ramsey’s baby steps, Step 6 involves paying off your home early. Personally, I have a different perspective on this step. However, I understand that many Asian cultures prioritize this step and often place it ahead of saving for retirement. The sense of freedom and relief that comes with being debt-free is indeed invaluable. Nonetheless, from a logical and analytical standpoint, I believe there might be a better return on investment if that money is used for other purposes, such as investing.

If you’ve purchased a house or refinanced your mortgage in the past decade, you’re likely aware that we’ve experienced historically low interest rates ranging from 2-3%.

Similar to what we discussed in Step 2, the decision to pay off your mortgage early depends on your mortgage interest rate. It becomes a comparison between a low-rate loan (e.g., 3%) and the potential returns of investing in a low-cost index fund like Vanguard’s VOO ETF, which has historically averaged around 10% per year.

Again, I emphasize that this suggestion is applicable only if you have a mindset and commitment to allocating the extra funds towards investing rather than paying off your mortgage. If you can’t commit to investing and find yourself using that money for discretionary expenses, then it’s advisable to focus on paying off your mortgage regardless of the interest rate being charged.

Step 7: Build wealth and give

I have to give props to Ramsey in using the words “building wealth” instead of say “get rich.” Being rich in my opinion means having a high income and or having a lot of cash. This however does not mean they have a positive net worth. We’ve all heard of professional sports players that make millions a year but unfortunately spend millions more. Having wealth in my opinion really doesn’t account for how much money you make, but really how much you spend of it. There was a story that I read that a janitor in Vermont that died with over $8 million in his account. I don’t care how much you made, I’d certainly call you wealthy if your net worth is over $8 million. Obviously, the key to the janitor building this wealth was his frugality (Asian trait).

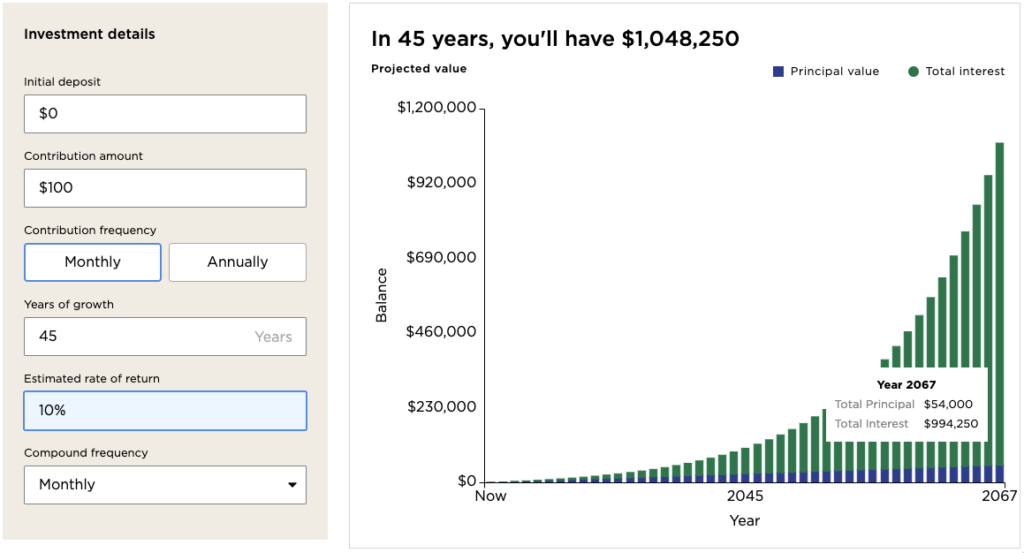

The way that I interpret Ramsey’s step 7 is similar to opening a brokerage account section in step 4, which is also the section I’m most geeked out at. If I had a time machine, I would revisit my 20yr old self and advise myself to make a $100 monthly purchase of the S&P500 index ETF (SPY or VOO) until I retire. Ideally investing more than $100 after my 30s and 40s but even if I stuck with $100/mo. After 45 years, that pot turns me into a millionaire while only investing a principal of $50k.

That my friend is truly how you build wealth which is also the secret sauce of the most famous investor in the world, Mr Warren Buffet.

In future blogs, I hope to write about all the naysayers out there that question how complicated it is, how they can’t afford it, it’s too late to do this, etc etc.

As for the giving part in Ramsey’s step 7, I fully respect this especially if you’ve reached step 7. The part that I would argue is that you really don’t have to wait until step 7 to give. Giving doesn’t always mean donating money. Giving could mean regularly giving blood, helping out a non-profit, coaching kids sports, walking for a cause, writing a blog hoping that you can affect 1 person, etc. Be creative. You’ll be surprised the sense of pride and comfort you’ll gain from this.